16 Simple Budget Check Ins to Do After the Holidays

The holidays can leave us feeling both joyful and financially stretched. Taking a moment to review your budget can help ease the stress and get you back on track. By examining your expenses, you can identify areas to save and adjust for the months ahead. Small steps now can make a big difference later.

This post may contain affiliate links, which helps keep this content free. Please read our disclosure for more info.

Review Your Holiday Spending

The holidays often lead to overspending, especially with gifts, travel, and festivities. Take the time to look over your holiday expenses and compare them with your planned budget. This will help you identify where you went over budget and understand why certain categories cost more than expected. By reviewing these numbers, you can adjust your expectations and allocate funds accordingly in the future.

Looking at your holiday spending now can also reveal patterns that may be worth addressing. For instance, you may notice that certain purchases were unnecessary or impulsive. This is a great opportunity to set better spending limits for next year and avoid financial stress. Understanding these patterns will help you approach next year’s budget with more control.

Update Your Emergency Fund

After the holiday season, it is essential to check in on your emergency fund. Review the current balance and assess whether it is enough to cover unexpected expenses, especially with the start of a new year. If your fund took a hit from holiday spending, make a plan to gradually replenish it. Setting aside a small portion of your monthly income can help rebuild this safety net over time.

A fully stocked emergency fund will give you peace of mind in case of job loss, medical bills, or car repairs. It is important to keep this fund separate from your regular savings to avoid spending it unintentionally. Start by setting a realistic goal for how much you need in the next few months, and prioritize building this reserve. Keeping your emergency fund at a healthy level will protect you from financial setbacks.

Assess Your Monthly Subscription Services

Subscription services like streaming platforms, meal kits, and gym memberships can quickly add up without you realizing. Take some time to evaluate each subscription and determine whether it is still serving you. Cancel any that are no longer necessary or used regularly to free up some budget. You may be surprised by how much money you can save by eliminating unused services.

It is a good idea to review your subscriptions periodically, especially after the holiday season when extra purchases may have added to your monthly expenses. This will help you identify areas where you can cut back and reallocate that money toward more important financial goals. Staying on top of subscriptions is an easy way to improve your budget without sacrificing much. Doing this regularly will keep your finances in check.

Track Your Credit Card Balances

After the holidays, many people find themselves carrying credit card balances from purchases made during the season. It is essential to track these balances and create a plan to pay them off as soon as possible. The longer you carry a balance, the more interest you will end up paying, which can make it harder to regain control of your finances. Start by reviewing your credit card statements and making a list of all balances.

Once you have an accurate picture of your credit card debt, prioritize paying off the highest-interest cards first. Consider transferring balances to a card with a lower interest rate, if available. Creating a plan to tackle these balances will prevent the debt from lingering throughout the year and ensure you do not carry holiday expenses into the next season. This is an important step to regain financial stability after the holidays.

Set New Financial Goals

After evaluating your spending, set new financial goals for the year ahead. Whether it is saving more for retirement, paying down debt, or building an investment portfolio, having clear goals will help you stay focused. Write these goals down and break them into smaller, manageable steps. Make sure to set realistic targets that can be achieved within your timeframe.

As the year progresses, revisit these goals to track your progress and adjust as needed. Having a defined goal will keep you motivated and on track. Use tools like budgeting apps or spreadsheets to monitor your progress and make adjustments along the way. Revisiting your goals will help you stay on course and make smarter financial decisions throughout the year.

Review Your Tax Withholdings

The beginning of the year is a good time to review your tax withholdings. This ensures that you are not under or overpaying your taxes throughout the year. Review your paycheck to see how much is being withheld for taxes, and make adjustments if necessary. If you received a large refund last year, it may be worth adjusting your withholdings to increase your monthly take-home pay.

Conversely, if you owed taxes last year, you may want to adjust your withholding to ensure you do not face a surprise tax bill. Speak with a tax professional or use online calculators to determine the optimal withholding amount for your situation. Staying on top of your tax situation throughout the year will prevent unnecessary stress when tax season comes around. It can also help you avoid surprises in your budget later.

Evaluate Your Savings Rate

A key factor in achieving financial success is saving regularly. After the holidays, check your savings rate and assess if it aligns with your long-term goals. If you have not been saving as much as you should, now is the time to start setting aside more. Consider automating your savings so that a portion of your income goes directly into a separate savings account each month.

A healthy savings rate can help you reach important goals, such as purchasing a home, building an emergency fund, or saving for retirement. Track your progress regularly to ensure that your savings are growing steadily. The earlier you start saving, the better prepared you will be for future financial needs. Make saving a priority, even in small amounts, to stay on track.

Reevaluate Your Housing Budget

Your housing expenses are likely one of your largest monthly costs, so it is important to review them after the holidays. Reassess your rent or mortgage payments and see if they are in line with your current budget. If you have experienced a change in income or have taken on additional debt, you may need to adjust your housing budget. Consider whether you can downsize, refinance, or find ways to reduce other housing-related expenses.

It is also a good idea to evaluate your utility costs and look for areas where you can cut back. Simple changes like adjusting your thermostat, reducing water usage, or switching to energy-efficient appliances can lower your monthly utility bills. By rethinking your housing budget, you may find that you have more money available for other financial goals. Staying on top of housing costs can help you maintain a healthy budget throughout the year.

Check Your Retirement Contributions

After the holiday season, it is important to check your retirement savings contributions. Are you on track to meet your long-term retirement goals? Consider increasing your contributions if possible, as doing so will help you build wealth for the future. If you have not started saving for retirement, now is the perfect time to open an account and begin contributing.

Review your retirement accounts and make sure your investments align with your goals and risk tolerance. Some retirement plans offer employer matching, so take full advantage of that benefit if it is available. Even small contributions can add up over time, and starting early gives you a better chance to secure a comfortable retirement. Checking your retirement contributions annually will keep you on track for long-term financial success.

Evaluate Your Debt Repayment Plan

Debt repayment can be one of the most significant financial hurdles. After the holidays, take a moment to review your existing debts, such as student loans, car payments, and credit card balances. Develop a clear strategy for paying off these debts and prioritize higher-interest accounts first. By organizing your debt repayment, you will create a clear path to becoming debt-free.

Consider making extra payments toward high-interest debt when possible, as this will help reduce the overall amount of interest you pay. Use a debt repayment calculator to figure out how long it will take to pay off each account and adjust your payments accordingly. Staying on top of your debt repayment will free up money for other financial goals in the future. Regularly evaluating your plan ensures that you stay focused on paying down your debt efficiently.

Adjust Your Monthly Budget

Now that the holidays are over, it is a good time to adjust your monthly budget for the upcoming year. Take a look at your income and expenses to see if any changes need to be made. If your holiday spending led to higher-than-expected bills, reallocate funds from other categories to help cover the shortfall. Creating a realistic monthly budget will ensure that you stay within your means.

Track your spending over the next few months to identify areas where you can reduce costs. Whether it is cutting back on dining out, reducing transportation costs, or eliminating unnecessary subscriptions, small adjustments can add up over time. Keep your budget flexible, so you can make changes as your financial situation evolves. An effective monthly budget helps you stay on track and avoid overspending.

Reflect on Your Financial Goals from Last Year

It is important to look back on your financial goals from the previous year to see what you accomplished. Did you reach the goals you set for yourself, such as saving for a down payment or paying off debt? Reflecting on these goals will help you understand what worked and what needs improvement. Consider setting new, more specific financial goals based on the lessons you have learned.

Reviewing your past goals can also motivate you to stay focused on your financial journey. Use this reflection as an opportunity to realign your priorities for the upcoming year. The more clearly you define your goals, the easier it will be to stay on track. Setting and achieving financial goals is a continuous process that helps you maintain financial security and peace of mind.

Set a Plan for Holiday Savings

The next holiday season will come sooner than you think, and planning ahead can prevent financial stress. Start a dedicated holiday savings fund now so that you can enjoy the season without the worry of overspending. Set a realistic monthly savings goal that will allow you to meet your holiday spending needs. You can automate the savings process to make it easier to stick to your plan.

By saving year-round, you will avoid the scramble of finding funds when the holidays roll around. This proactive approach ensures that you will have enough for gifts, travel, and entertainment without putting your finances in jeopardy. Holiday savings can also help you stick to your budget and avoid resorting to credit cards for seasonal expenses. Begin now and enjoy a financially stress-free holiday season next year.

Keep Track of Large Purchases

It is important to keep track of any large purchases you make throughout the year. Whether it is a new car, appliance, or home improvement project, such purchases should be factored into your overall budget. Plan ahead for these big expenses by setting aside funds in advance. This will help you avoid putting too much strain on your budget when it is time to make the purchase.

Consider breaking large purchases into smaller, manageable payments if possible. This can help you manage your cash flow and reduce the impact on your budget. Keeping track of major expenses ensures that they do not catch you off guard and that you can make informed decisions. It is essential to factor these expenses into your budget to avoid unnecessary financial stress.

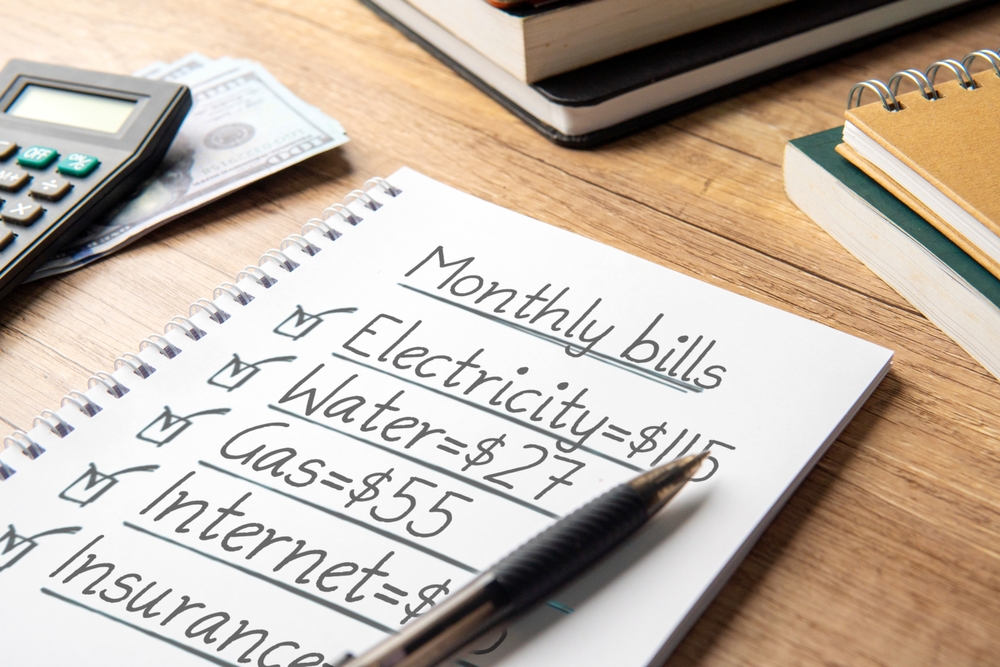

Automate Bill Payments

One of the easiest ways to stay on top of your budget is to automate your bill payments. Setting up automatic payments for recurring expenses like utilities, mortgage or rent, and insurance ensures that they are always paid on time. This prevents late fees and helps you stay organized. You can choose to automate payments for both fixed and variable expenses to simplify your finances.

Automating payments also saves time, as you will not need to manually track due dates or worry about missed payments. Be sure to monitor your bank account regularly to ensure that funds are available for these automated transactions. Over time, automation can reduce your financial stress and help you stay on top of your budget. It is a simple but effective way to manage your finances with minimal effort.

Track Your Spending for the Next Few Months

After reviewing your budget, commit to tracking your spending over the next few months. This practice will give you a clear understanding of where your money is going and help you make adjustments as needed. You can use budgeting apps or a simple spreadsheet to monitor your expenses. By doing this, you can quickly identify areas where you may be overspending or where you can cut back.

Tracking your spending also helps you stay accountable to your financial goals. This regular review will give you insight into your habits and allow you to make better choices moving forward. The more you track your spending, the easier it becomes to make informed financial decisions. Keeping a close eye on your budget will help you stay on track and avoid financial surprises.

This article originally appeared on Avocadu.